MAP Views Second Quarter 2026

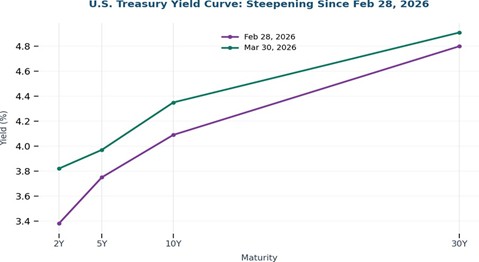

Apr 01, 2026Stocks began the first quarter much as they ended 2025. Notably, foreign equities and currencies outperformed domestic equities and the U.S. dollar. However, global stock markets retreated in March as the oil complex and the dollar rallied following the start of the conflict in the Middle East. U.S. markets were not immune, as the S&P 500 declined for four consecutive weeks heading into the end of the quarter before a last-day rally, marking its worst quarter since 2022. As tensions surrounding the conflict increased, so too did concerns about a potentially weakening economy. Contrary to historical precedent—when domestic yields typically decline during geopolitical conflict—interest rates instead rose, as depicted by the green line in the chart below.

Source: U.S. Treasury; Reconstructed using constant-maturity yields as of February 28, 2026 and March 30, 2026.

Rising inflationary pressures—driven by surging energy prices, renewed supply-chain disruptions tied to geopolitical conflict, and persistent labor-cost growth—combined with the growing possibility of a recession have once again placed the Federal Reserve (the Fed) in a difficult position. At the beginning of the year, Wall Street consensus was for the Fed to cut rates twice during 2026, despite the Fed’s internal expectations for one cut. With inflation risks on the rise, the confidence of those bets has waned over the past few weeks, with some on Wall Street now expecting the Fed’s next move could be a rate hike.

Unlike most other countries’ central banks whose sole mandate is price stability, the Fed operates under a dual mandate that includes both price stability and full employment. Those two mandates can, at times, come into conflict. Sustained full employment can increase household income and demand, which may place upward pressure on prices. Historically, the 2-year Treasury note often moves ahead of Fed funds rate changes, reflecting how markets price future hikes or cuts before the Federal Open Market Committee acts. When yields on the 2-year Treasury note fall, it usually indicates that the Fed will cut rates; conversely, rising yields often foreshadow higher policy rates. However, given the current economic uncertainty stemming from geopolitical tensions and lingering questions regarding how artificial intelligence may disrupt labor markets, we question whether this historical relationship will hold.

The Fed is designed to be politically independent. But with the Chair of the Fed nominated by the President and confirmed by the Senate, independence does not mean detachment. We believe the Fed is likely to opt for the politically preferred choice of lowering interest rates. During times of uncertainty, as the old saying goes, people would rather pay more for goods and services if it means having a job. We contend such action would steepen the yield curve, as short-term yields (i.e., Treasury bills and money market instruments) decline while longer-dated yields move higher.

Our expectation of a steepening yield curve is supportive of the Investment Team’s belief that there is greater risk than reward at the longer end of the interest rate curve. As a result, we continue to emphasize shorter-maturity bonds in portfolios containing fixed-income investments. Fixed income portfolios do not hold any bonds with maturities beyond 2029, and the weighted average maturity is just below 1.5 years. This disciplined positioning helps reduce exposure to interest rate swings, insulating clients from the duration risk associated with owning longer-dated bonds.

While the ongoing conflict in the Middle East has increased the risk of a recession in recent weeks, recession is not our baseline forecast. That said, it is nearly impossible to predict with any accuracy how long the conflict will last. Short-duration conflicts limit fiscal and inflationary impacts, whereas prolonged conflicts create a greater risk of recession. This uncertainty lends itself to volatility.

Whenever volatility increases, investors inevitably ask the question: “Why not transition to cash until this is resolved?” Such a strategy rarely works. As an example, in the first quarter of 2020 when COVID-19 was grinding the economy to a virtual halt and stocks were tumbling, many investors suggested moving to cash “until a cure was found.” Despite the lack of a cure, stocks pivoted and rebounded sharply in response to unprecedented global fiscal and monetary stimulation. This point is further evidenced by the fact that missing just the 10 best days in the stock market over the past 30 years would have reduced your returns by more than 50%. If you can successfully pick the 10 best days out of 30 years, you are incredibly lucky and should probably buy lottery tickets. History also shows that market bottoms often occur when headlines are dominated by the most pessimistic narratives.

Rather than attempting to time the resolution of the Middle East conflict, we remain committed to a disciplined approach focused on owning quality companies trading at attractive valuations with solid dividend yields. We remain overweight in the consumer staples and healthcare sectors, which have historically performed well during periods of economic weakness. We are also overweight in the materials sector. Although the rationale has shifted modestly in light of recent geopolitical developments, we continue to believe commodities are in the early innings of a bull market. Conversely, we remain significantly underweight in the financials sector reflecting ongoing concerns about conditions in the private credit market.

First-quarter performance was encouraging and reflected the strength of MAP’s investment process in a market that continues to reward patience and selectivity. While short-term results are not the primary objective, this period underscores the advantages of remaining focused on value and long-term fundamentals amid shifting market sentiment. As always, we remain committed to prudent capital allocation, rigorous research, and thoughtful risk management, as we strive to deliver the best risk-adjusted returns possible.

Thank you for your continued trust and partnership.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, and Nicolas Vilotti

April 1, 2026

Certain statements made by us may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent a recommendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell, or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change.