The ‘Cockroach’ Theory Explained: Private Credit Had Better Purchase Raid® by the Shipping Container Full

Mar 16, 2026In the world of stock market investing, there is a belief that when a company reveals one negative surprise, investors assume more problems are likely hiding beneath the surface—just like seeing one cockroach suggests there are many more you cannot see yet.

We believe the cockroach theory is unfolding in the dwelling of private credit. Private credit is, by design, illiquid. Loans are not traded on open markets, and investors often face long lock-up periods with limited avenues for exit. In stable markets, this rigidity can feel manageable. In stressed markets, it can become a trap. The illusion of “stability” can therefore create complacency—right up until the moment repricing becomes unavoidable. More on that a bit later, but first, a history lesson.

Prior to the Great Financial Crisis (GFC), the private credit space was relatively small and primarily isolated to the institutional world (public pension funds, hedge funds, family offices, endowments, etc.). Over the past several years, however, private credit has reached the mainstream. Lured by the prospect of potentially higher returns, lower volatility, and so-called non-correlation with other asset classes, retail investors gained exposure to private credit. Retail investors held 16.6% of private credit funds at the end of 2024, up from just 5.5% in 2020.

A prolonged period of historically low interest rates in traditional fixed-income markets helped fuel the shift toward private credit. After the GFC, and the regulatory changes that followed, the size of the private credit market swelled. The Dodd-Frank Act of 2010, enacted with the intent of strengthening financial stability, increased traditional bank capital and liquidity requirements, enhanced oversight, and sought to limit risky activities. While it reduced risk-taking within traditional banks, these stricter rules also curtailed bank lending, creating an opening for non-bank lenders and accelerating the growth of the private credit market.

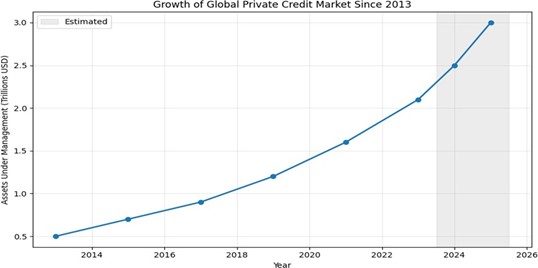

Source: IMF Global Financial Stability Report Data and BIS analysis

Globally, based on current data, private credit is estimated to be between $2.0 and $3.0 trillion, up nearly fourfold since 2013, with the U.S. accounting for roughly 70% to 75% of the market.

Following this post-GFC driven rise, default rates in private credit reached 9.2% in 2025,1 up from 3.6% at the end of 2020 and above peak COVID stress rates of 8.1%.2 In what has become a case study in the risks of opaque private credit structures, in September 2025, First Brands Group, a major U.S. automotive aftermarket parts manufacturer best known for brands such as FRAM, Raybestos, TRICO, Autolite, and Centric filed for Chapter 11 bankruptcy protection under a cloud of fraud investigations. The firm had pursued aggressive, debt-funded transactions using private credit over the prior decade, leaving it highly levered and increasingly dependent on complex financing structures. Several large institutions disclosed hundreds of millions of dollars of exposure, with recovery values highly uncertain due to disputed collateral priority and missing assets.

Subsequent events provide further evidence of mounting risk:

- In February and again in March, Blue Owl Capital announced a fundamental shift in how it provides liquidity to shareholders, particularly for its non-traded business development company, Blue Owl Capital Corporation II (OBDC II). The company arranged a $1.4 billion sale of direct lending assets, including $600 million from OBDC II, to manage investor payouts and debt, with sales occurring near par value. This is concerning for many reasons, one of which is the high volume of retail investors in their private credit funds.

- On March 5, 2026, BlackRock slashed the value of a $25 million private loan to Infinite Commerce Holdings down to zero after assessing it at 100 cents on the dollar just three months While relatively small for a firm such as BlackRock, the speed at which the value of the loan collapsed is baffling and evokes memories of Bear Stearns and Lehman Brothers—both of which were rated investment grade shortly before their downfall.

- On March 11, 2026, investors in Cliffwater LLC’s flagship private credit fund sought to redeem approximately 14% of their shares during the first quarter, leading the firm to cap repurchases of the $33 billion fund at 7%.

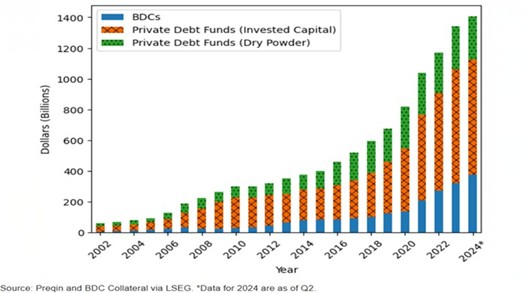

Unfortunately, despite post-GFC regulations, banks are not immune to the problems boiling up in the private credit markets. Instead of lending directly to borrowers, banks have lent to Business Development Companies (BDCs), publicly regulated investment companies in the U.S. that provide financing to small-and mid-sized businesses. These businesses can be more vulnerable to economic cycles, earnings volatility, limited collateral quality, and disruptions in supply chains or consumer demand. Moody’s estimates that U.S. banks have lent approximately $1.2 trillion to non-depository financial institutions, of which about $300 billion are loans to private credit providers and a comparable amount to private equity providers.

We believe our portfolios are constructed to weather the private credit storm. We do not own private debt directly, equity or debt investments in any BDCs, nor do we own any bank stocks. One advantage of being a high-conviction manager is the ability to be highly selective—not only in where we invest, but equally in where we choose not to. As we discussed in a previous Thought Piece, we have not owned traditional bank stocks since 2007. Not many investment managers can make that claim.

We do not believe the woes of the private credit space will permeate the financial sector the way subprime mortgages did in 2008, but we do expect more pain in the coming months. While we intend to watch this unfold from the sidelines, we remain attentive to the associated risks. The bottom line is that we believe public markets are superior to private markets. Public markets offer higher levels of transparency and liquidity. As mentioned at the beginning of this piece, during times of uncertainty, these are two desirable attributes that private markets lack.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, and Nicolas Vilotti

March 2026

1Fitch Ratings’ U.S. Private Credit (PMR) Portfolio

2Proskauer Private Credit Default Index

Certain statements made by us may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent a recommendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell, or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change.