The Illusion of Diversification

Jul 09, 2026As the markets cross into the second half of 2026, the contrast between MAP’s global value strategies and the mainstream benchmarks has rarely been starker. In this Thought Piece, we expand on the structural distortion in the markets discussed in MAP Views Third Quarter that we believe represents both a considerable hidden risk for passive index investors and a profound opportunity for disciplined value investors.

Ask the average investor, “What is the S&P 500 index?” and they would probably respond something along the lines of: “a well-diversified portfolio of iconic American companies.” In fact, today, that response is merely an illusion of the past. The index has reached a level of concentration that eclipses the peak of the 1990’s dot-com bubble and the Nifty Fifty from the early 1970s.

A striking 40% of the index is concentrated in just ten holdings. If you own a standard capitalization-weighted S&P 500 index fund, you are not buying a diversified portfolio; you are simply making an outsized bet on a small group of mega-cap technology and semiconductor companies.

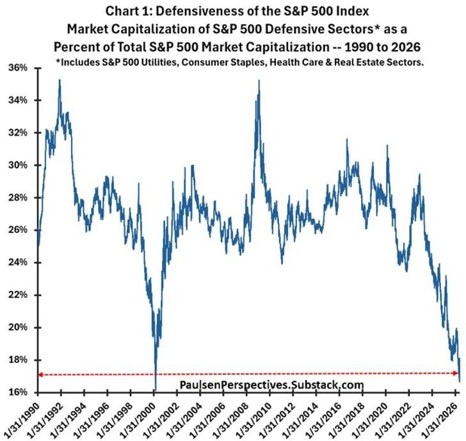

While capital has crowded into technology stocks, it has flowed out of defensive sectors. Such sectors include consumer staples, health care, utilities, and real estate investment trusts. These businesses are often less exciting than the market’s current growth leaders, but they can serve an important role in a portfolio because their revenues are typically tied to recurring, essential demand: food and household products, electricity and water, medical care, prescription drugs, and long-duration property assets. In periods when economic growth slows, interest-rate expectations shift, or investor risk appetite fades, these sectors have historically provided balance relative to more cyclical or valuation-sensitive parts of the market. As the chart below illustrates, defensive industries now comprise only 17% of the S&P 500 Index, compared with 36% during the market bottom of the Great Financial Crisis. This means that the S&P 500 index may appear broadly diversified, while in fact the index offers far less inclusion of the very sectors that have traditionally helped investors in the index weather market stress.

Interestingly, the last time the defensiveness of the index was this low was in the first quarter of 2000, which coincided with the peak of the dot-com bubble.

NVIDIA alone has a market capitalization greater than that of all consumer staples and utilities stocks combined in the S&P 500 index. The comparison becomes even more striking when viewed alongside the other largest market capitalization names in the benchmark. NVIDIA, Apple, Microsoft, Amazon, Alphabet, Broadcom, Meta Platforms, Tesla, and Berkshire Hathaway together account for a disproportionate share of the index’s total value, with most of that weight concentrated in technology, semiconductors, digital advertising, cloud computing, e-commerce, and AI-related infrastructure. Several of these companies are exceptional businesses with dominant competitive positions, but their collective size means that the performance of the S&P 500 index is increasingly tied to a narrow set of growth expectations. For passive investors, this creates a subtle but important risk: an index that appears diversified across 500 companies may, in practice, be driven by the earnings results, valuation multiples, and investor sentiment surrounding a relatively small group of mega-cap stocks.

History suggests that market concentration can stretch only so far before reversing. When leadership rotates—as recent volatile trading sessions may be signaling—the shift away from crowded mega-cap stocks and toward overlooked value sectors can happen swiftly. For example, imagine a trading day when investors begin questioning whether AI-related capital spending can continue at its recent pace. In that environment, the largest technology and semiconductor stocks could decline sharply as valuation multiples compress, pulling the capitalization-weighted S&P 500 lower even if most companies in the index are relatively stable. At the same time, investors may rotate toward consumer staples, utilities, health care, and other value-oriented businesses because their earnings are less dependent on aggressive growth assumptions. The result is a market that looks weak at the index level, but underneath the surface shows meaningful outperformance from the very sectors that had been neglected during the prior period of mega-cap leadership.

We are not suggesting that investors eliminate technology exposure. We maintain positions in the technology sector, including in select Magnificent Seven companies and semiconductors, but believe we diversification and disciplined position sizing are essential. Artificial intelligence is real, and many technology companies offer meaningful growth potential, but price still matters. Paying extreme valuation premiums leaves little margin for operational missteps or shifts in technology spending or the broader economy. We believe the technology stocks we own are attractive due to a combination of growth potential, moats around their businesses, and impressive operating metrics.

In short, there is no substitute for having a well-conceived, diversified portfolio.

Please reach out to your MAP representative with any questions or if we can be of assistance.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, Zachary Fellows, and Nicolas Vilotti

July 2026

Certain statements made by us may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. The information contained herein represents our views as of the aforementioned date and does not represent a recommendation by us to buy or sell this security or any other financial instrument associated with it. Managed Asset Portfolios, our clients and our employees may buy, sell, or hold any or all of the securities mentioned. We are not obligated to provide an update if any of the figures or views presented change.