Your Portfolio on Politics

Jul 24, 2020We are now less than four months away from the U.S. elections. Things have changed since our last analysis. We are due for an update.

The Democrats have the momentum going into the final stretch. COVID-19 and its fallout have put a significant damper on the Trump campaign. The administration’s response has been negatively received and has effectively neutralized the Republicans’ most effective talking point: the economy. Markets have taken well to rapid legislative and Fed-driven stimulus, but middle- and low-income households have felt the brunt of the pandemic.

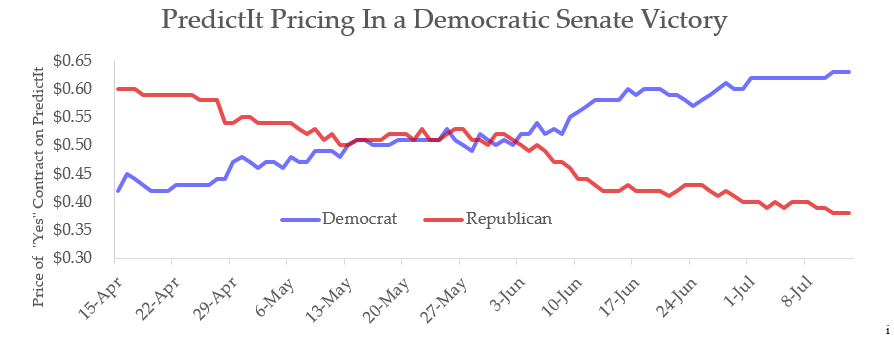

Democratic control of the Senate – which seemed unlikely as recently as March – has become the odds-on favorite outcome for betting markets:

The odds of a Democratic victory in the House has seen a similar rise, and presidential polls are tipping heavily in Joe Biden's favor.

The 2016 elections proved that polls and public opinion could be wrong, and in politics and markets, nothing is a guarantee. Democrats recall the "silent majority" that elevated Donald Trump into office. As Biden continues to poll as much as 10-15% ahead of the incumbent Trump, remember: we are more than 100 days from the election, and Hillary Clinton was heavily favored to win on election night 2016. Further, Biden has yet to announce his running mate in an election where the Democratic vice-presidential candidate will matter more than usual: both candidates are septuagenarians in the time of coronavirus. The race is still very much up in the air.

While the Democrats have become the favorite in the polls, some political and financial talking heads have grown concerned that a victory for Democrats would spell trouble for markets. Giving fuel to the fear is Joe Biden's apparent leftward drift following the Democratic primary -- a trend that runs counter to the normal moderation seen post-primary. The $2 trillion climate plan recently floated by the Biden campaign has its roots in the "Green New Deal," making energy execs and investors queasy.

Some of the drift left is undoubtedly an attempt to energize the unenthused group of young liberals whose preferred candidate was Bernie Sanders. Slightly easing concerns is that any proposed plans will have to run the congressional gauntlet, sanding down the more radical edges. Additionally, the effects of the ruling party on the stock market are often overblown: specific sectors will get dinged based on the winning administrations' policies, but severe market crashes should not be forecasted based on the party in power.

However, it would be foolish to completely ignore critical policies that can affect asset prices. We examine the tax policies and coronavirus response proposed by both candidates. These should be the main public policy concerns for investors in the coming years.

Tax Policy

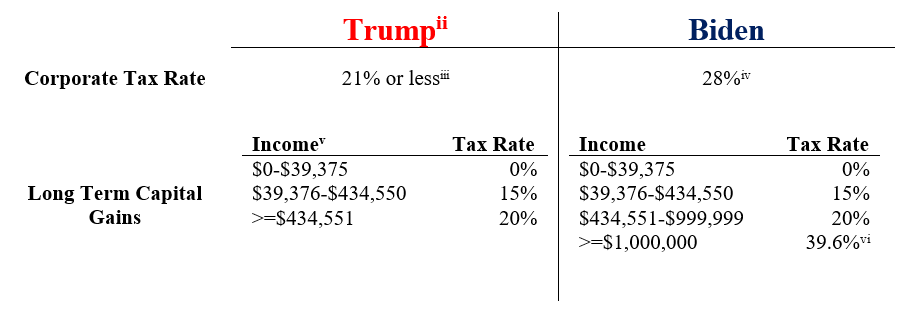

In Trump's first term, we saw significant tax reform. The corporate tax rate was cut from 35% to 21%, helping to drive the bull market during the first three years of the administration. The two most relevant issues to investors are corporate tax rate and long-term capital gains:

Finance media has looked on fearfully as Joe Biden has partnered up with Wall Street bogeyman Bernie Sanders. Senator Sanders has earned -- and is assuredly proud of -- his reputation for intimidating big business and billionaires.

While the Sanders partnership may help motivate young people to the polls for Biden in November, the proposals are not particularly radical. The 28% corporate tax rate floated by the Biden campaign is still less than the 35% in place at the beginning of the Trump administration, and the bump in Long-Term Capital Gains rates would only affect the richest of Americans.

However, a 33% rise in the corporate tax rate would place stress on already stretched valuations and COVID-depressed earnings. The 2020 P/E ratio for the S&P 500 is hovering around 25x. Under a 28% tax regime, the 2020 P/E would be around 28.5x, further pushing markets into overstretched territory on a valuation basis. Combined with potential long-term damage from the pandemic dampening earnings into 2021 and 2022, this could result in lackluster returns for U.S. markets.

Panic is not justified, but, understandably, investors would be concerned about a Democratic sweep and its potential tax implications. Under Joe Biden's 28% proposal, earnings theoretically drop about 9%. Not catastrophic, but not negligible.

Coronavirus Response

As investment advisors, we are not in any position to tell you the correct health measures to be taken in response to COVID-19. Ideally, we reopen the country safely and as quickly as possible. There are two keywords there: safely and quickly. Large portions of the population will continue to avoid public places even if they are open while the virus is still spreading. The economy will not be able to open at full tilt until the virus is mostly controlled.

Europe has seen some pent up demand get unleashed as hard-hit countries ease restrictions, and case numbers remain low. Germany and Ireland, two countries which have primarily contained the virus are seeing restaurants return to normal in the restaurant sector:

Trump and Biden have competing views on how to reopen. Trump is trying to convince the public that the threat of illness from coronavirus is insufficient to shut down our schools and businesses, while Biden has touted a complete shut down until the virus is contained. Public perception of safety is what matters to the economy. Until people feel safe going out, businesses that rely on close human interaction will continue to suffer.

On the stimulus front, the bipartisanship on the economic measures taken in response to COVID-19 has been encouraging. Even in our combative political environment, unprecedented financial relief programs were approved that have helped ease the troubles of U.S. businesses and families.

There are early rumblings of disagreement over the next round of stimulus, but they seem to be over smaller details. Lessons learned from the first set of bills around the size of unemployment checks and income cutoffs for employees will be incorporated. Disagreements will pop up over who deserves stimulus, and the parties will have different opinions on the split between business and individual aid. However, both parties seem to be determined to help the economy stay above water and recover. This is likely to continue regardless of who is elected in November.

Stay in the Game?

Political rhetoric will ramp up as we head into another emotionally charged election season. The media will continue to provide their takes, and pundits will attempt to convince the public that a vote for the other team will spell disaster for the markets.

The effects of the party in power have historically been muted. Market timing is difficult or even impossible to do, and the US public equities chart for the last century has generally been up and to the right. We will continue to focus on the long term and attempt to reduce the noise created by political and financial pundits. We believe this is the best way to pursue long term returns.

Remember: stock index futures contracts tanked when it became clear that Donald Trump would win the presidency. The market is up over 50% in the nearly four years since. Investors should avoid knee jerk reactions come November 3rd.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, John Dalton, Zack Fellows

Research and analysis by Dustin Dieckmann

July 2020

The information contained herein does not represent a recommendation by us to buy or sell any security or securities mentioned within this presentation. Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. Past performance is no guarantee of future results.

i https://www.cnbc.com/2020/06/29/biden-tells-donors-he-will-end-most-of-trumps-tax-cuts.html

ii Current tax policy under Trump administration.

iv https://www.cnbc.com/2020/06/29/biden-tells-donors-he-will-end-most-of-trumps-tax-cuts.html

vii https://www.opentable.com/state-of-industry. 2/18/2020-7/19/2020.