Is The Market Underestimating Long-Term Inflation Risk?

May 27, 2020China-U.S. tensions have been rising. Governments worldwide have jumped in to fill the economic gaps left by COVID-19. The Fed’s money printers have certainly been… whirring?

The worst pandemic in 100 years has shaken up economies, markets, and geopolitics. During world-changing events, people clamor to predict long- and short-term ramifications. 2020 is no different. An old debate has once again gained steam as the first round of stimulus gives way to a potential second: inflation. The familiar cast of characters are on their respective sides. There are those who believe the massive amount of money added to the system by the U.S. Federal Reserve will inevitably lead to inflation – even hyperinflation. Others point to the mild inflation after then-unprecedented monetary stimulus during the Great Financial Crisis as evidence of more upcoming mild inflation.

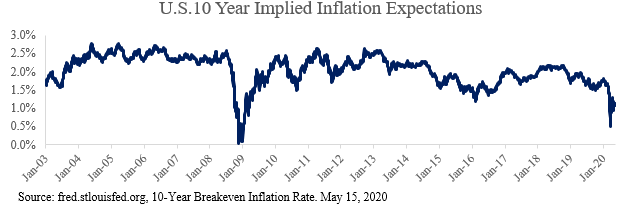

Both sides raise fair points. It is notoriously difficult to predict macroeconomic factors like inflation. However, it is clear what the market thinks:

Inflation expectations are as low as they have been since 2009. This is not a ridiculous proposition: the drop in demand caused by lockdowns, among other factors, creates near-term deflationary pressures. However, several key factors may lead to inflation after the effects of the pandemic subside. We examine the issue more closely:

What causes inflation?

The key determinant of inflation is the balance of supply and demand. “Demand-Pull” inflation occurs when a hot economy causes consumers to demand more products, thus “pulling” the price up. “Cost-Push” inflation is its counterpart: an increase in the cost of producing a good or service, “pushing” up prices throughout the supply chain.

During a recession, deflationary pressures often prevail. As consumers lose their jobs and income, demand for goods and services drops and so do prices, while supply is readily available to produce more. Expansions are more commonly associated with inflation: supply capacity becomes stretched, and producers can raise their prices due to increased demand.

The Set-Up

We are seeing the steepest drop in employment since The Great Depression. People are spending less and saving more. Deflationary. In fact, because of the economic shock stemming from coronavirus, we will likely see deflation during the next two to three years. The Federal Reserve and the federal government know how to treat this: economic stimulus. The last thing the country wants to see is deep deflation – deflation causes consumers to spend fewer dollars and can end up spiraling out of control (see: Great Depression).

To combat deflation, the federal government has stepped in with massive amounts of stimulus. In fact, the stimulus is so large that some unemployed workers are reluctant to return to work due to the size of their unemployment benefits. They simply make more money not working.

The Federal Reserve has printed reams of digital dollars during the pandemic, with the M2 money supply increasing over 20% Y/Y during the crisis. Alongside this, target interest rates have been dropped to effectively 0%. The Fed has signaled it has “unlimited” buying power.

Meanwhile, tensions have been ratcheting up between D.C. and Beijing. The trade war that had been ebbing is renewed. A war of words has been started. The Trump administration believes anti-China rhetoric is a winning formula for the upcoming election. The Chinese Communist Party must save face and deflect blame to the U.S. to maintain support for their authoritarian government. As these tensions have escalated, many countries have begun pulling manufacturing and business out of China causing a shift away from the cheap labor that has been employed in the past few decades.

Near-Term and Long-Term Inflation

The deflationary effects of unemployment are more than enough to offset near-term increases in government spending. As households and companies recover from the coronavirus, spending will be stingy. This shock is unique because consumers are not just unable to spend, they are afraid to go out. Demand will be down due to fear of the virus, further adding to deflationary pressures.

However, the long term (2 years or more) environment could be set up for a return to inflation levels not seen since the 1970s.

The Demand Pull: Consumers and workers will now expect the government to apply heavy-handed intervention during economic downturns. This will lead to more spending. Much of the finance community believes the financial scare of coronavirus is going to push consumers to save. In the near term that is likely true. But, we continue to believe human nature and the U.S. culture will return to its historical ways. Additionally, the massive increase in money supply will mean more money chasing after goods and services. Inflationary.

The Cost Push: The developed world has been relying on cheap labor from foreign suppliers for years. China has provided a large portion of this. It is more likely than not that U.S.-China tensions worsen. The already frayed relations have only been further irritated by the COVID-19 outbreak. U.S. and foreign companies are already beginning to shift production out of China. This is a lasting trend. Some industries will be required to shift production to safer pastures: pharmaceuticals, critical infrastructure technology, and other goods necessary to the safety of the United States. Other companies will shift voluntarily to de-risk their supply chain from tariffs or otherwise. The long-term effect is an increase in prices as companies no longer take advantage of China’s cheap labor.

Once inflation starts, it is painful to stop. The steps that must be taken include higher interest rates and tighter monetary policy. This can cause recession and pain for everyone, including and especially those in the middle and lower class. In a world where there has been rising populism and politicians who are willing to do whatever it takes to get elected, it will be highly difficult to stop runaway inflation.

There are no certainties in investing or economics. Inflation is no exception. However, long-term inflation is more likely than the market is currently discounting. Responsible money managers will consider these risks and adjust accordingly. For now, we will continue to keep the duration of the bonds we purchase short, and as always we will strive to find companies that provide great risk/reward characteristics. MAP will continue to search for hidden risks and adjust its portfolios accordingly.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, John Dalton, Zack Fellows

Research and analysis by Dustin Dieckmann

May 2020

Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. Past performance is no guarantee of future results.