83 Tons Of Fraudulent Gold

Aug 06, 2020The last few months have continued to cement our conviction to avoid investment in China-based companies. The Senate passed a bill that could force the delisting of China-based stocks on U.S. exchanges.(i) The anti-CCP rhetoric has been ratcheted up to a fever pitch as November approaches. And yet more Chinese companies have faced allegations of fraud. Put simply: investing in China-based companies is a perilous endeavor. Screening out geographies with inadequate corporate governance and financial controls is essential to Managed Asset Portfolios’ process.

A new fraud emerged in the wake of Luckin Coffee and TAL Education. Kingold Jewelry, a U.S.-listed Chinese jeweler, put up 83 tons of gold as collateral for $2.8 Billion in loans from numerous financial firms. However, fraud was uncovered when a bank attempted to seize their collateral after Kingold defaulted on its debt. The 83 tons of gold turned out to be merely gilded copper – worth significantly less than the solid gold counterpart.

If you’re having trouble picturing what 83 tons of fraudulent gold looks like, below is a one-ton water buffalo made of (purportedly) real solid gold. 83 of these:

As a general principle, Managed Asset Portfolios attempts to avoid minefields.Chinese equities represent one of the most extensive minefields in the investment landscape. Because of the lack of proper regulatory oversight, fraud will be a continuous problem in Chinese companies.

Fraud isn’t the only issue…

Since our last piece, the trade and verbal spat between the U.S. and China has been simmering. Between mixed messages from either government, one thing is clear:the relationship has been souring. Some of the events that have transpired since our last paper:

• The Senate passed a bill disqualifying Chinese companies from being listed on U.S. exchanges. While it is not a direct ban, it would require foreign companies to follow U.S. standards for audits and other financial regulations – something China is very reluctant to allow.

• A travel ban is being considered for Chinese Communist Party members – numbered around 90 million. The CCP runs the Chinese government.

• In a sign that the U.S. is gaining international traction in their quest against Chinese tech, the U.K. banned Huawei equipment from their 5G infrastructure. Additionally, companies and governments are growing increasingly concerned about TikTok, a social media app feared by many as being capable of surveillance on behalf of the CCP. President Trump signed an executive order forcing the company to sell its U.S. operations, or lose its ability to generate revenue in the U.S. Government agencies have already taken steps to ban the app, and some companies have begun asking employees to avoid using the app.

As tensions intensify, technology and geopolitical analysts are growing increasingly concerned over Taiwan’s position as the leading manufacturer of semiconductors – the building blocks of computers and modern life. Semiconductors power everything from smartphones to missile systems. China’s recent power grab in Hong Kong is worrying to Taiwan’s future, and thus the future of semiconductor supply to the western world. Watch for any movement on this front in the coming months.

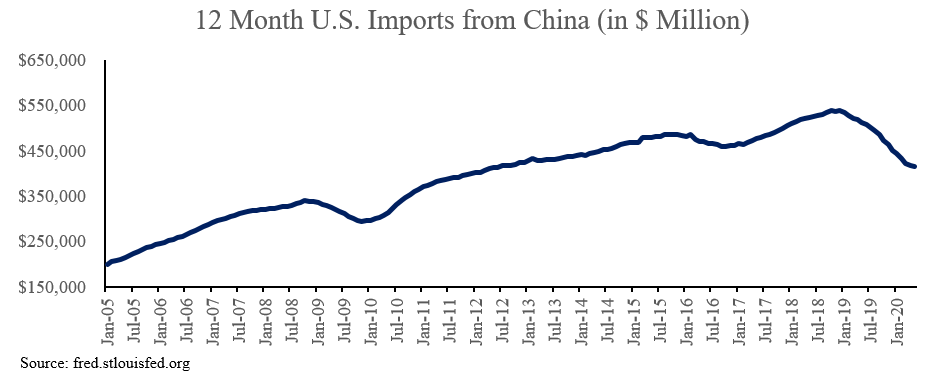

U.S. and Chinese leaders understand that the two countries still need each other. The U.S. relies on China for labor and manufacturing, while China needs the Western World’s money to support its debt-laden economy. A sharp cutoff in relations would be unwise, making it unlikely that the situation deteriorates rapidly. However, the U.S. and China had already begun curtailing bilateral trade before the pandemic. U.S. imports from China fell about 17% year-over-year in 2019, before the bulk of the effects of the pandemic.

A gradual decoupling will be painful for both economies. However, if non-Chinese companies gradually shift production out of China, the U.S. will likely be the relative winner. It will take work, but so did setting up the supply chain in China. If China loses foreign demand for its labor, it will not be easy to replace. We think the adverse effects on China will be far more severe than the impact in the U.S.

Additionally, U.S. companies have been complaining for years about Chinese companies undercutting their prices in domestic markets. The price slashing companies are often accused of receiving governmental aid allowing them to offer significantly lower prices in non-Chinese markets. Victims of the underpricing would be grateful for a reduction in competition on the lower end of the price spectrum.

Businesses and consumers benefited from increased globalization, and will likewise suffer in the short-term as supply chains get rerouted and new labor must be trained. There are usually no true winners in significant economic shake-ups, but the U.S. is better positioned to face a decoupling.

Stay Vigilant

As the situation progresses, keep an eye out for potential signs of deteriorating relationships, including:

• Power grabs in Taiwan: The long-disputed status of Taiwan has made it a flashpoint for tensions in the region. Semiconductor giant Taiwan Semiconductor produces around half of the world’s outsourced chips.(ii) The U.S. and China cannot allow an adversary to gain control of this production.

• U.S. ban on CCP members: Politicians will continue to say that the problem is not the Chinese people, but the Chinese Communist Party. A move to ban anyone associated with the CCP would keep nearly 1 in 15 Chinese citizens from coming to the U.S.

• Breaking of the U.S.-China “Phase 1” trade deal: This deal is still ostensibly in place, but it is hanging by a thread. Ripping up the deal would mean capitulation on the future of friendly trade relations between the two superpowers.

We will continue to monitor the progression of U.S.-China tensions and position our portfolios accordingly. The situation is constantly evolving. Just as we published this piece, the White House announced its support of the Senate bill passed in May. It appears that the U.S. may require Chinese companies to comply with U.S. audit standards. Given the abundance of frauds the public has faced, this is long overdue.

While we believe direct investment in Chinese companies to be unwise, it would be foolish to avoid revenue exposure to China. The Chinese market has been a leader in global growth for multiple decades, and many U.S. and foreign companies will continue to benefit from growing consumption in China. Companies which sell into China but are regulated outside of the country can offer a unique opportunity for investors: they benefit from the growth in the economy, while simultaneously having a more watchful eye as a regulator.

Investors should use caution: market indexers could find that they have more exposure to China than they thought. China represents nearly 41% of the MSCI Emerging Markets Index as of June 30, 2020.(iii) Investors must know what they are buying when they invest passively.

China will have its share of success stories, but the lack of corporate governance creates an environment ripe for fraud. We continue to search for opportunities elsewhere.

Managed Asset Portfolios Investment Team

Michael Dzialo, Karen Culver, Peter Swan, John Dalton, Zack Fellows

Research and analysis by Dustin Dieckmann

August 2020

The information contained herein does not represent a recommendation by us to buy or sell any security or securities mentioned within this presentation. Certain statements may be forward-looking statements and projections which describe our strategies, goals, outlook, expectations, or projections. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied by such forward-looking statements. Past performance is no guarantee of future results.

______________________________________________

i https://www.bbc.com/news/business-52749801

ii https://fortune.com/2020/07/28/intel-7nm-delay-tsmc-stock-shares-worlds-tenth-most-valuable-company/